Agriculture is the lifeblood of Pakistan’s economy. It contributes 23.5% to gross domestic product (GDP) and employs over 37% of the labour force, with 70% of the rural population depending on it for their livelihoods. Pakistan’s agricultural sector comprises livestock (64%), crops (33%), fisheries (1.3%) and others (1.7%). This insight focuses on the crop sub-sector with particular emphasis on the ‘important crops’ to identify the challenges and prospects for revitalising Pakistan’s agriculture sector.

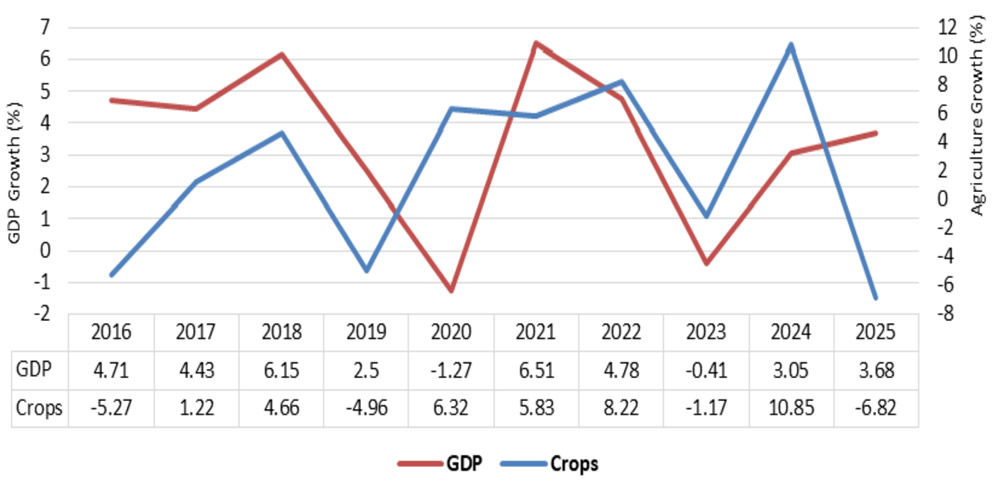

In 2025, Pakistan’s crop subsector declined by 6.82% compared to 2005. Figure 1 indicates that the combined annual growth rate of the crops subsector has remained lower (1.7%) than the population growth rate (2.55%) from 2016 to 2025. The widening demand-production gap intensifies food insecurity and forces costly imports. Therefore, evaluating crop yield gaps, despite their smaller share, is essential to revitalise the agriculture sector.

Figure 1: GDP and Agricuture Growth (2016-2025)

Source: Economic Survey of Pakistan and Pakistan Bureau of Statistics (PBS)

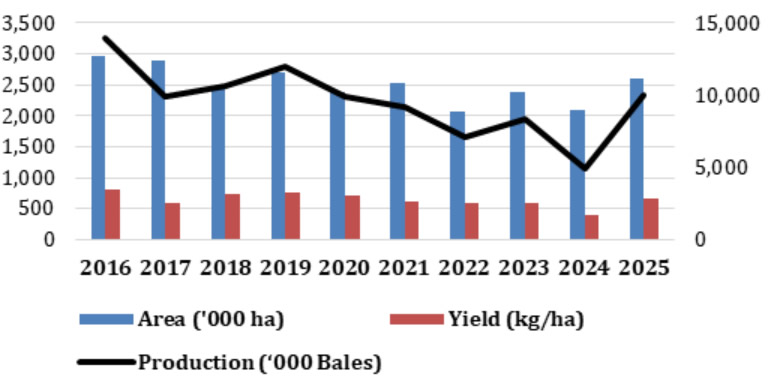

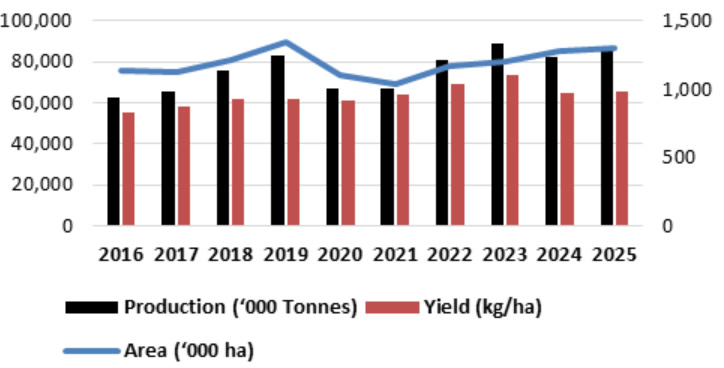

Within the crop sub-sector, cotton, maize, rice, sugarcane, and wheat are considered ‘important crops’ because they contribute 4.19% to GDP. Cotton’s cultivated area has decreased by 12% (from 2.96 to 2.60 million hectares), and production has reduced by 28% (from 13.96 to 10 million bales) from 2016 to 2025 (Figure 2). The decline in area, production, and yield is attributed to poor seed quality, pest pressure, and reduced profitability, which compels farmers to prematurely terminate cotton after one picking.

Figure 2: Cotton - Area, Production and Yield

Source: Adapted from PBS

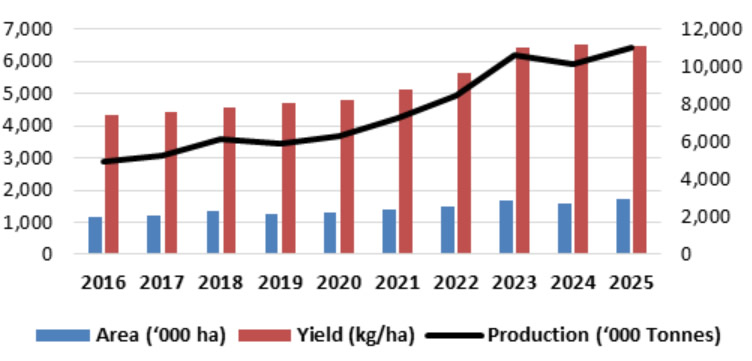

Maize has shown consistent growth over the last 10 years. Figure 3 indicates that the cultivated area increased by 49% (from 1.14 to 1.7 million hectares) and total production grew by 123% (from 4.9 to 11 million tonnes) from 2016 to 2025. A 50% increase in yield per hectare suggests that farmers treat maize as a flexible option, likely switching to it based on market conditions.

Figure 3: Maize - Area, Production and Yield

Source: Adapted from PBS

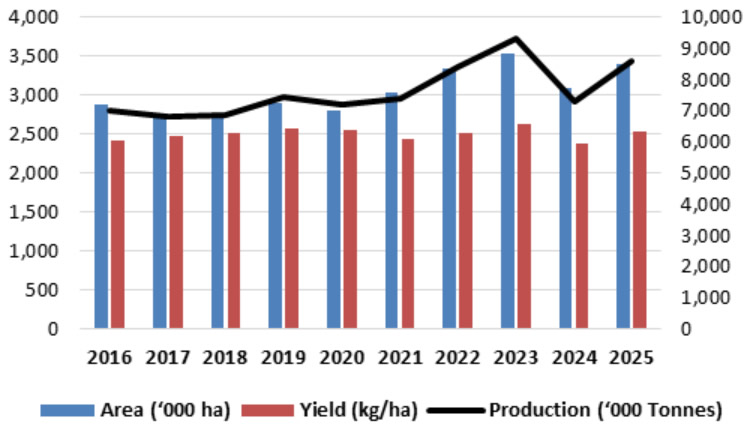

Rice’s cultivated area has increased by 18%, and total production rose by 23% from 2016 to 2025, as shown in Figure 4. The 4% increase in yield per hectare shows moderate growth.

Figure 4: Rice - Area, Production and Yield

Source: Adapted from PBS

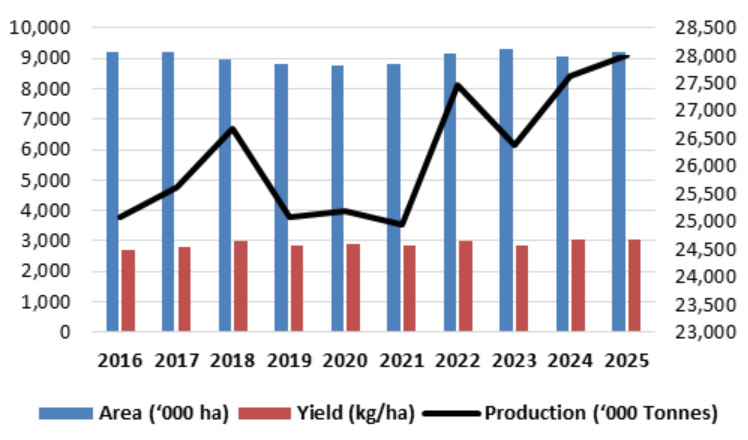

Sugarcane’s cultivated area has increased by 14%, and total production rose by 35% from 2016 to 2025, as depicted in Figure 5. 18% increase in per-hectare yield demonstrates that sugarcane is a reliable and productive crop for the sugar industry, though its water-intensive nature remains a significant vulnerability.

Figure 5: garcane - Area, Production and Yield

Source: Adapted from PBS

Wheat production has increased slightly from 25 to 28 million tonnes, while cultivated area has remained unchanged from 2016 to 2025, as shown in Figure 6. Despite rising population demand, this stagnation in wheat production is associated with poor seed quality and policy gaps.

Figure 6: Wheat - Area, Production and Yield

Source: Adapted from PBS

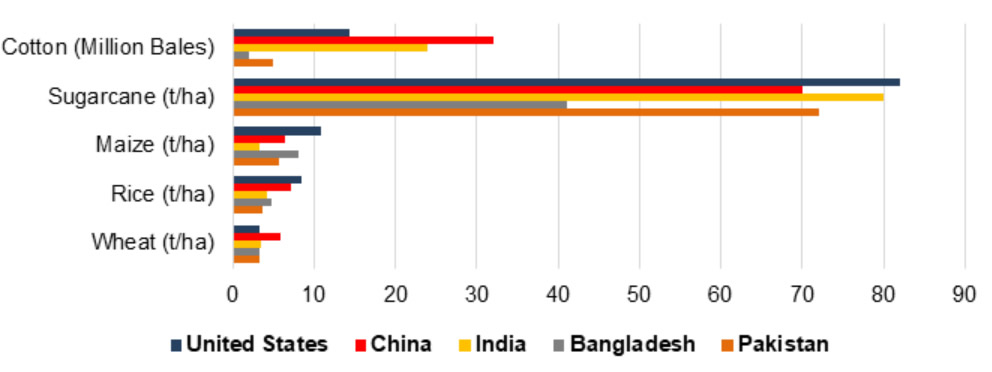

The global yield data (Figure 7) confirms low productivity in Pakistan. Pakistan’s 3.2 tons/hectare (t/ha) wheat yield, sugarcane yield (72 t/ha) and cotton output (5 million bales) fall short of India and China. In contrast, maize yield (5.7 t/ha) is higher than India’s (3.2 t/ha). Low yield in Pakistan is attributed to limited financing and traditional farming.

Figure 7: Global Yield Comparison

Source: Adapted from the US Department of Agriculture

The data above shows an imbalance in the important crops. The production of water-intensive sugarcane and rice is increasing, putting more pressure on depleting water resources. In contrast, production of strategically vital wheat and cotton is stagnating or declining, posing a critical risk to food security and the textile industry. The existing research shows that seed and pesticide quality, fertiliser costs, technology adoption, and access to finance are the fundamental barriers undermining wheat and cotton production.

Certified seed production meets only 35.6% of national demand (742,000 MT against 2.09 million MT), while 95% of wheat area still relies on old varieties.

Available pesticides are less effective against pink bollworm, whitefly, and cotton leaf curl virus, resulting in cotton yield losses.

The fertiliser prices for urea (from Rs 1400 to 4400) and DAP (from Rs 2500 to 13500) have increased manifold from 2016 to 2025, reducing farmers’ ability to maintain recommended application rates.

The government has launched several initiatives to address structural weaknesses in the crop subsector. First, the seed and input reforms include the Seed Act 2024, seed testing by the National Seed Development and Regulatory Authority (NSDRA), action against substandard suppliers, and expansion of certified seed production. The seed policy was tightened through registration, inspections and 268 court cases against substandard dealers in 2025.

Second, policy interventions include the Prime Minister’s Agriculture Emergency Programme (PM-AEP), Kisan Card, machinery subsidies, low-interest credit, agricultural research and water infrastructure investments. During 2005-2025, the agricultural research budget has increased from 0.1% to 0.2% of GDP.

Third, the import of agricultural machinery has increased (from US$ 45 million to US$85.7 million) from 2016 to 2025, due to subsidies. Likewise, agricultural credit increased from Rs 600 billion to Rs 2,580 billion from 2016 to 2025.

The above interventions indicate that the state is focusing on structural reforms, yet the “important crops” are increasingly imbalanced as water-intensive sugarcane and rice expand (Figures 4-5), but wheat stagnates (Figure 6) and cotton contracts (Figure 2), deepening risks to food security and the textile value chain. The global comparison (Figure 7) further suggests that Pakistan’s core problem is persistent yield gaps driven by weak input, high production costs, and low technology.

Pakistan’s crop growth remains below population growth, reflecting persistent yield gaps. Agricultural productivity can be revitalised through a paradigm shift from “more spending” to “more productivity per rupee and per drop”.

This “productivity-first package” includes certified inputs, targeted incentives, and water-smart cropping. A practical way forward is converting credit and subsidies into “smart finance” by linking support to certified inputs and measurable adoption of modern practices to enhance yield gains. However, this requires enforcement capacity and coordination among all stakeholders.

Pakistan doesn’t lack initiatives. It lacks enforcement and incentives aligned with productivity. If executed with capacity and coordination, this package can reverse the yield gap, reduce import pressure, stabilise the textile base, and protect rural livelihoods.